2026 Q1 -tulosraportti

98 päivää sitten

‧32 min

1,00 NOK/osake

Viimeisin osinko

3,68%Tuotto/v

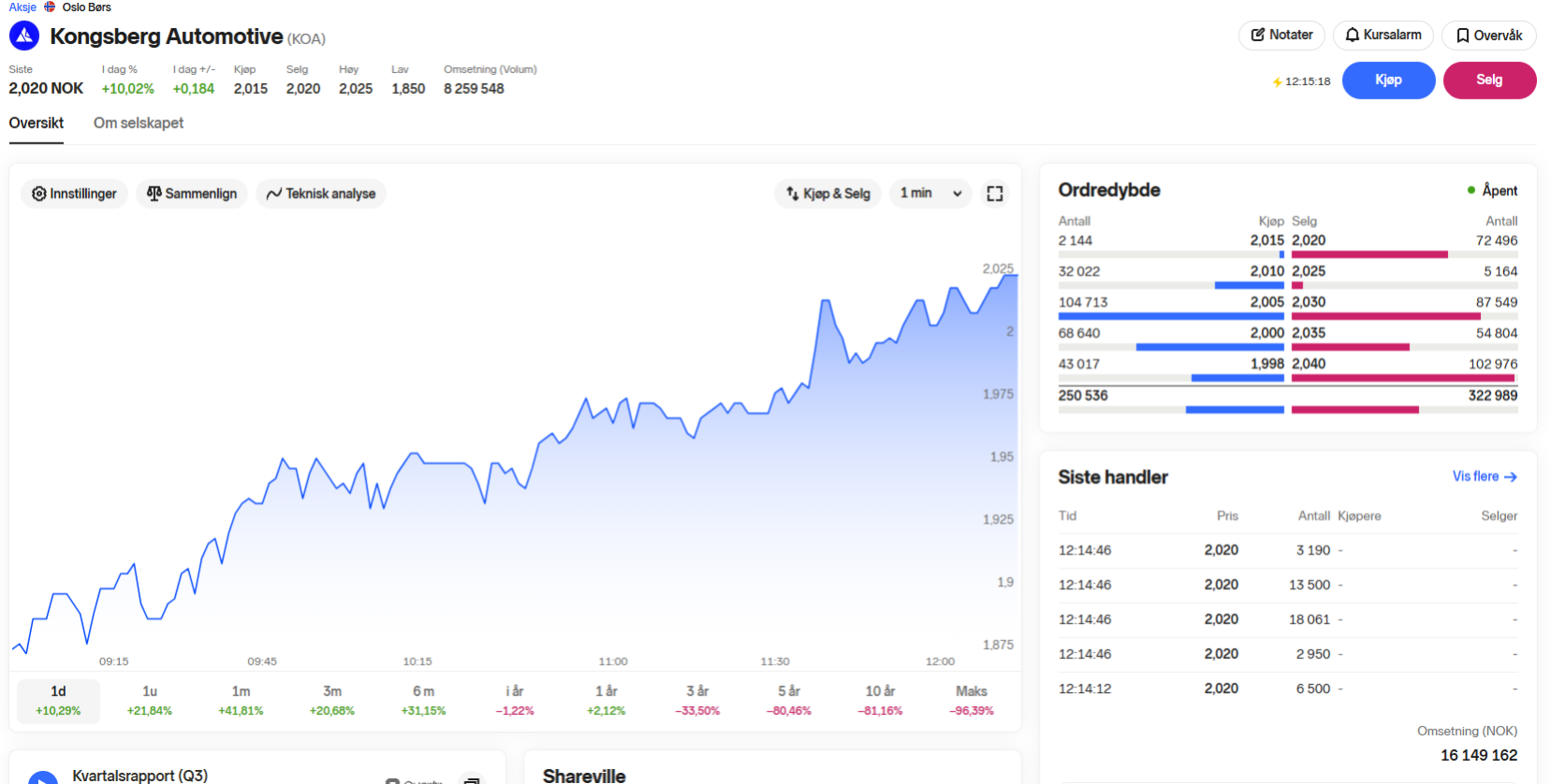

Tarjoustasot

Ei dataa

Viimeisimmät kaupat

| Aika | Hinta | Määrä | Ostaja | Myyjä |

|---|---|---|---|---|

| - | - | - | - |

Huomioi, että vaikka osakkeisiin säästäminen on pitkällä aikavälillä tuottanut hyvin, tulevasta tuotosta ei ole takeita. On olemassa riski, että et saa sijoittamiasi varoja takaisin.

Välittäjätilasto

Dataa ei löytynyt

Yhtiötapahtumat

Datan lähde: Quartr| Seuraava tapahtuma | |

|---|---|

2026 Q2 -tulosraportti 13.8. | 2 päivää |

| Menneet tapahtumat | ||

|---|---|---|

2026 Q1 -tulosraportti 5.5. | ||

2025 Q4 -tulosraportti 12.2. | ||

2025 Q3 -tulosraportti 6.11.2025 | ||

2025 Q2 -tulosraportti 14.8.2025 | ||

2025 Q1 -tulosraportti 7.5.2025 |

Asiakkaat katsoivat myös

Foorumi

Liity keskusteluun Nordnet Socialissa

Kirjaudu

·28.7.Nice rise lately, is it starting to get expensive now?

·28.7.Nice rise lately, is it starting to get expensive now? In the big picture, it hasn't moved much since they went public, -and what a company it has built these years! In addition, the management has bet 100% correctly when it comes to steering the company towards security and interoperability instead of a video service. That will show in the numbers going forward.

In the big picture, it hasn't moved much since they went public, -and what a company it has built these years! In addition, the management has bet 100% correctly when it comes to steering the company towards security and interoperability instead of a video service. That will show in the numbers going forward. ·26.7.E24 (24.7.): Pexip is number 49 on the list showing the 50 stocks with the largest upside to analysts' average price target. Only companies with at least five analysts are included. https://e24.no/boers-og-finans/i/WvJqak/aksjene-med-stoerst-oppside-paa-oslo-boers 41 Paratus Energy Services 6 47,50kr 57,25kr 20,5 % 42 Multiconsult 7 151,40kr 181,00kr 19,6 % 43 Europris 8 84,10kr 100,40kr 19,4 % 44 Hafnia 10 73,35kr 87,50kr 19,3 % 45 Bouvet 5 44,20kr 52,50kr 18,8 % 46 SATS 8 40,00kr 47,50kr 18,8 % 47 Mowi 16 198,40kr 235,00kr 18,4 % 48 BlueNord 8 529,00kr 626,29kr 18,4 % 49 Pexip 6 77,60kr 90,83kr 17,0 % 50 Klaveness Combination Carriers 6 98,90kr 113,32kr 14,6 %The first 20: 1 Hexagon Composites 5 10,01kr 16,88kr 68,6 % 2 Magnora 6 23,70kr 36,83kr 55,4 % 3 Salmon Evolution 8 4,05kr 6,24kr 54,1 % 4 Akastor 6 13,12kr 19,83kr 51,1 % 5 Panoro Energy 9 29,05kr 43,80kr 50,8 % 6 Capital Tankers 5 124,04kr 180,71kr 45,7 % 7 Ventura Offshore 7 29,40kr 42,47kr 44,5 % 8 Nordic Aqua Partners 5 78,80kr 113,00kr 43,4 % 9 Komplett 5 6,72kr 9,63kr 43,3 % 10 Odfjell Technology 7 60,04kr 82,83kr 38,0 % 11 BW Energy 7 54,70kr 75,00kr 37,1 % 12 SED Energy Holdings 7 8,03kr 10,95kr 36,4 % 13 Vend Marketplaces 19 230,00kr 311,74kr 35,5 % 14 Scatec 11 96,90kr 131,09kr 35,3 % 15 Bonheur 8 226,50kr 306,25kr 35,2 % 16 Link Mobility 9 25,08kr 33,84kr 34,9 % 17 Norbit 6 175,00kr 235,33kr 34,5 % 18 Kongsberg Gruppen 11 291,80kr 392,36kr 34,5 % 19 Bruton 7 54,40kr 72,60kr 33,5 % 20 Constellation Oil Services 7 140,00kr 186,57kr 33,3 %

·26.7.E24 (24.7.): Pexip is number 49 on the list showing the 50 stocks with the largest upside to analysts' average price target. Only companies with at least five analysts are included. https://e24.no/boers-og-finans/i/WvJqak/aksjene-med-stoerst-oppside-paa-oslo-boers 41 Paratus Energy Services 6 47,50kr 57,25kr 20,5 % 42 Multiconsult 7 151,40kr 181,00kr 19,6 % 43 Europris 8 84,10kr 100,40kr 19,4 % 44 Hafnia 10 73,35kr 87,50kr 19,3 % 45 Bouvet 5 44,20kr 52,50kr 18,8 % 46 SATS 8 40,00kr 47,50kr 18,8 % 47 Mowi 16 198,40kr 235,00kr 18,4 % 48 BlueNord 8 529,00kr 626,29kr 18,4 % 49 Pexip 6 77,60kr 90,83kr 17,0 % 50 Klaveness Combination Carriers 6 98,90kr 113,32kr 14,6 %The first 20: 1 Hexagon Composites 5 10,01kr 16,88kr 68,6 % 2 Magnora 6 23,70kr 36,83kr 55,4 % 3 Salmon Evolution 8 4,05kr 6,24kr 54,1 % 4 Akastor 6 13,12kr 19,83kr 51,1 % 5 Panoro Energy 9 29,05kr 43,80kr 50,8 % 6 Capital Tankers 5 124,04kr 180,71kr 45,7 % 7 Ventura Offshore 7 29,40kr 42,47kr 44,5 % 8 Nordic Aqua Partners 5 78,80kr 113,00kr 43,4 % 9 Komplett 5 6,72kr 9,63kr 43,3 % 10 Odfjell Technology 7 60,04kr 82,83kr 38,0 % 11 BW Energy 7 54,70kr 75,00kr 37,1 % 12 SED Energy Holdings 7 8,03kr 10,95kr 36,4 % 13 Vend Marketplaces 19 230,00kr 311,74kr 35,5 % 14 Scatec 11 96,90kr 131,09kr 35,3 % 15 Bonheur 8 226,50kr 306,25kr 35,2 % 16 Link Mobility 9 25,08kr 33,84kr 34,9 % 17 Norbit 6 175,00kr 235,33kr 34,5 % 18 Kongsberg Gruppen 11 291,80kr 392,36kr 34,5 % 19 Bruton 7 54,40kr 72,60kr 33,5 % 20 Constellation Oil Services 7 140,00kr 186,57kr 33,3 %- ·23.7.Thought about topping up a bit, but it looks like it dips in the afternoon lately, so maybe it's just as well to wait until this pattern is broken…

Yllä olevat kommentit ovat peräisin Nordnetin sosiaalisen verkoston Nordnet Socialin käyttäjiltä, eikä niitä ole muokattu eikä Nordnet ole tarkastanut niitä etukäteen. Ne eivät tarkoita, että Nordnet tarjoaisi sijoitusneuvoja tai sijoitussuosituksia. Nordnet ei ota vastuuta kommenteista.

Uutiset

Tämän sivun uutiset ja/tai sijoitussuositukset tai otteet niistä sekä niihin liittyvät linkit ovat mainitun tahon tuottamia ja toimittamia. Nordnet ei ole osallistunut materiaalin laatimiseen, eikä ole tarkistanut sen sisältöä tai tehnyt sisältöön muutoksia. Lue lisää sijoitussuosituksista.

2026 Q1 -tulosraportti

98 päivää sitten

‧32 min

1,00 NOK/osake

Viimeisin osinko

3,68%Tuotto/v

Uutiset

Tämän sivun uutiset ja/tai sijoitussuositukset tai otteet niistä sekä niihin liittyvät linkit ovat mainitun tahon tuottamia ja toimittamia. Nordnet ei ole osallistunut materiaalin laatimiseen, eikä ole tarkistanut sen sisältöä tai tehnyt sisältöön muutoksia. Lue lisää sijoitussuosituksista.

Foorumi

Liity keskusteluun Nordnet Socialissa

Kirjaudu

- ·28.7.Nice rise lately, is it starting to get expensive now?In the big picture, it hasn't moved much since they went public, -and what a company it has built these years! In addition, the management has bet 100% correctly when it comes to steering the company towards security and interoperability instead of a video service. That will show in the numbers going forward.

- ·26.7.E24 (24.7.): Pexip is number 49 on the list showing the 50 stocks with the largest upside to analysts' average price target. Only companies with at least five analysts are included. https://e24.no/boers-og-finans/i/WvJqak/aksjene-med-stoerst-oppside-paa-oslo-boers 41 Paratus Energy Services 6 47,50kr 57,25kr 20,5 % 42 Multiconsult 7 151,40kr 181,00kr 19,6 % 43 Europris 8 84,10kr 100,40kr 19,4 % 44 Hafnia 10 73,35kr 87,50kr 19,3 % 45 Bouvet 5 44,20kr 52,50kr 18,8 % 46 SATS 8 40,00kr 47,50kr 18,8 % 47 Mowi 16 198,40kr 235,00kr 18,4 % 48 BlueNord 8 529,00kr 626,29kr 18,4 % 49 Pexip 6 77,60kr 90,83kr 17,0 % 50 Klaveness Combination Carriers 6 98,90kr 113,32kr 14,6 %The first 20: 1 Hexagon Composites 5 10,01kr 16,88kr 68,6 % 2 Magnora 6 23,70kr 36,83kr 55,4 % 3 Salmon Evolution 8 4,05kr 6,24kr 54,1 % 4 Akastor 6 13,12kr 19,83kr 51,1 % 5 Panoro Energy 9 29,05kr 43,80kr 50,8 % 6 Capital Tankers 5 124,04kr 180,71kr 45,7 % 7 Ventura Offshore 7 29,40kr 42,47kr 44,5 % 8 Nordic Aqua Partners 5 78,80kr 113,00kr 43,4 % 9 Komplett 5 6,72kr 9,63kr 43,3 % 10 Odfjell Technology 7 60,04kr 82,83kr 38,0 % 11 BW Energy 7 54,70kr 75,00kr 37,1 % 12 SED Energy Holdings 7 8,03kr 10,95kr 36,4 % 13 Vend Marketplaces 19 230,00kr 311,74kr 35,5 % 14 Scatec 11 96,90kr 131,09kr 35,3 % 15 Bonheur 8 226,50kr 306,25kr 35,2 % 16 Link Mobility 9 25,08kr 33,84kr 34,9 % 17 Norbit 6 175,00kr 235,33kr 34,5 % 18 Kongsberg Gruppen 11 291,80kr 392,36kr 34,5 % 19 Bruton 7 54,40kr 72,60kr 33,5 % 20 Constellation Oil Services 7 140,00kr 186,57kr 33,3 %

- ·23.7.Thought about topping up a bit, but it looks like it dips in the afternoon lately, so maybe it's just as well to wait until this pattern is broken…

Yllä olevat kommentit ovat peräisin Nordnetin sosiaalisen verkoston Nordnet Socialin käyttäjiltä, eikä niitä ole muokattu eikä Nordnet ole tarkastanut niitä etukäteen. Ne eivät tarkoita, että Nordnet tarjoaisi sijoitusneuvoja tai sijoitussuosituksia. Nordnet ei ota vastuuta kommenteista.

Tarjoustasot

Ei dataa

Viimeisimmät kaupat

| Aika | Hinta | Määrä | Ostaja | Myyjä |

|---|---|---|---|---|

| - | - | - | - |

Huomioi, että vaikka osakkeisiin säästäminen on pitkällä aikavälillä tuottanut hyvin, tulevasta tuotosta ei ole takeita. On olemassa riski, että et saa sijoittamiasi varoja takaisin.

Välittäjätilasto

Dataa ei löytynyt

Asiakkaat katsoivat myös

Yhtiötapahtumat

Datan lähde: Quartr| Seuraava tapahtuma | |

|---|---|

2026 Q2 -tulosraportti 13.8. | 2 päivää |

| Menneet tapahtumat | ||

|---|---|---|

2026 Q1 -tulosraportti 5.5. | ||

2025 Q4 -tulosraportti 12.2. | ||

2025 Q3 -tulosraportti 6.11.2025 | ||

2025 Q2 -tulosraportti 14.8.2025 | ||

2025 Q1 -tulosraportti 7.5.2025 |

2026 Q1 -tulosraportti

98 päivää sitten

‧32 min

Uutiset

Tämän sivun uutiset ja/tai sijoitussuositukset tai otteet niistä sekä niihin liittyvät linkit ovat mainitun tahon tuottamia ja toimittamia. Nordnet ei ole osallistunut materiaalin laatimiseen, eikä ole tarkistanut sen sisältöä tai tehnyt sisältöön muutoksia. Lue lisää sijoitussuosituksista.

Yhtiötapahtumat

Datan lähde: Quartr| Seuraava tapahtuma | |

|---|---|

2026 Q2 -tulosraportti 13.8. | 2 päivää |

| Menneet tapahtumat | ||

|---|---|---|

2026 Q1 -tulosraportti 5.5. | ||

2025 Q4 -tulosraportti 12.2. | ||

2025 Q3 -tulosraportti 6.11.2025 | ||

2025 Q2 -tulosraportti 14.8.2025 | ||

2025 Q1 -tulosraportti 7.5.2025 |

1,00 NOK/osake

Viimeisin osinko

3,68%Tuotto/v

Foorumi

Liity keskusteluun Nordnet Socialissa

Kirjaudu

- ·28.7.Nice rise lately, is it starting to get expensive now?In the big picture, it hasn't moved much since they went public, -and what a company it has built these years! In addition, the management has bet 100% correctly when it comes to steering the company towards security and interoperability instead of a video service. That will show in the numbers going forward.

- ·26.7.E24 (24.7.): Pexip is number 49 on the list showing the 50 stocks with the largest upside to analysts' average price target. Only companies with at least five analysts are included. https://e24.no/boers-og-finans/i/WvJqak/aksjene-med-stoerst-oppside-paa-oslo-boers 41 Paratus Energy Services 6 47,50kr 57,25kr 20,5 % 42 Multiconsult 7 151,40kr 181,00kr 19,6 % 43 Europris 8 84,10kr 100,40kr 19,4 % 44 Hafnia 10 73,35kr 87,50kr 19,3 % 45 Bouvet 5 44,20kr 52,50kr 18,8 % 46 SATS 8 40,00kr 47,50kr 18,8 % 47 Mowi 16 198,40kr 235,00kr 18,4 % 48 BlueNord 8 529,00kr 626,29kr 18,4 % 49 Pexip 6 77,60kr 90,83kr 17,0 % 50 Klaveness Combination Carriers 6 98,90kr 113,32kr 14,6 %The first 20: 1 Hexagon Composites 5 10,01kr 16,88kr 68,6 % 2 Magnora 6 23,70kr 36,83kr 55,4 % 3 Salmon Evolution 8 4,05kr 6,24kr 54,1 % 4 Akastor 6 13,12kr 19,83kr 51,1 % 5 Panoro Energy 9 29,05kr 43,80kr 50,8 % 6 Capital Tankers 5 124,04kr 180,71kr 45,7 % 7 Ventura Offshore 7 29,40kr 42,47kr 44,5 % 8 Nordic Aqua Partners 5 78,80kr 113,00kr 43,4 % 9 Komplett 5 6,72kr 9,63kr 43,3 % 10 Odfjell Technology 7 60,04kr 82,83kr 38,0 % 11 BW Energy 7 54,70kr 75,00kr 37,1 % 12 SED Energy Holdings 7 8,03kr 10,95kr 36,4 % 13 Vend Marketplaces 19 230,00kr 311,74kr 35,5 % 14 Scatec 11 96,90kr 131,09kr 35,3 % 15 Bonheur 8 226,50kr 306,25kr 35,2 % 16 Link Mobility 9 25,08kr 33,84kr 34,9 % 17 Norbit 6 175,00kr 235,33kr 34,5 % 18 Kongsberg Gruppen 11 291,80kr 392,36kr 34,5 % 19 Bruton 7 54,40kr 72,60kr 33,5 % 20 Constellation Oil Services 7 140,00kr 186,57kr 33,3 %

- ·23.7.Thought about topping up a bit, but it looks like it dips in the afternoon lately, so maybe it's just as well to wait until this pattern is broken…

Yllä olevat kommentit ovat peräisin Nordnetin sosiaalisen verkoston Nordnet Socialin käyttäjiltä, eikä niitä ole muokattu eikä Nordnet ole tarkastanut niitä etukäteen. Ne eivät tarkoita, että Nordnet tarjoaisi sijoitusneuvoja tai sijoitussuosituksia. Nordnet ei ota vastuuta kommenteista.

Tarjoustasot

Ei dataa

Viimeisimmät kaupat

| Aika | Hinta | Määrä | Ostaja | Myyjä |

|---|---|---|---|---|

| - | - | - | - |

Huomioi, että vaikka osakkeisiin säästäminen on pitkällä aikavälillä tuottanut hyvin, tulevasta tuotosta ei ole takeita. On olemassa riski, että et saa sijoittamiasi varoja takaisin.

Välittäjätilasto

Dataa ei löytynyt